Job Support Scheme which is further split into JSS Open and JSS Closed is available from 1st November and it will run for 6 months for employees on the payroll on 23rd Sep.

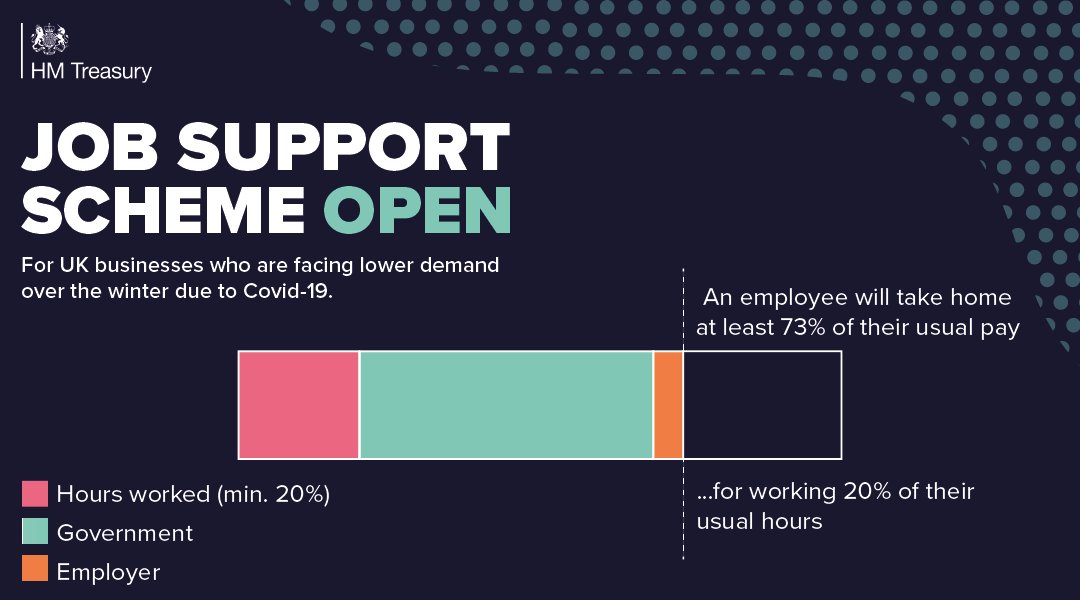

Job Support Scheme Open (JSS Open)

Are you employed by a business that is still open? You’ll need to work at least 20% of your hours to be eligible for anything under ‘JSS – Job Support Scheme Open’.

This is different from the original furlough scheme, under which you weren’t allowed to work at all. Now you must work at least 20% of normal hours (originally 33% before last week’s change).

If you hit that minimum you’ll get 73% of your normal wage, up to a cap (see below) – but the more you work, the more you get. It works like this:

- – Your employer will pay you as normal for the hours you work.

- – Your employer pays 5% and the state 62% of your remaining wage, with the state’s part capped at £1,542/mth. Then you lose the rest.

Job Support Scheme Closed (JSS Closed)

Are you employed by a business forced to close due to lockdown? Most should get 67% of their wage from the state under ‘Job Support Scheme Closed’.

This is a new element to help businesses, branches or departments instructed to close, but it won’t cover those that choose to close themselves.

That 67% is capped at £2,083/mth, while your employer must cover pension and national insurance but it doesn’t have to pay any wages.

There are a number of conditions that apply to all employers using the Job Support Scheme. The conditions apply to all employers claiming JSS Open and JSS Closed unless stated.

Conditions of Claiming Job Support Scheme

There are a number of conditions that apply to all employers using the Job Support Scheme. The conditions apply to all employers claiming JSS Open and JSS Closed unless stated.

Redundancy

Employers cannot claim for an employee who has been made redundant or is serving a contractual or statutory notice period during the claim period.

The government expects that large employers (250 or more employees) and their corporate groups using the scheme will not make capital distributions whilst claiming the Job Support Scheme grant. This includes:

- – dividend

- – charge

- – free or other distribution

- – any equivalent payment that a partnership may make to its partners

The government does not plan to make this expectation a contractual or legal condition of the scheme but encourages business to reflect on their responsibilities and that taxpayers should be able to rely on public money only being claimed where it is clearly needed.

Paying employee taxes and pension contributions

The Job Support Scheme grant will not cover National Insurance contributions (NICs) or pension contributions. These contributions remain payable by the employer.

Employers must deduct and pay to HMRC income tax and employee NICs on the full amount that is paid to the employee, including any amounts subsequently met by a scheme grant.

Employers must also pay to HMRC any employer NICs due on the full amount that that is paid to the employee, including any amounts subsequently met by a scheme grant.

Employers must report these payments via a Full Payment Submission (FPS) to HMRC on or before the pay date in the normal way.

Employers and Employees must also still pay pension contributions in accordance with the applicable pension scheme terms unless the employee has opted out or stopped saving into their pension. If applicable Student Loan deductions and the Apprenticeship Levy must also still be paid.

Grant monies must only reimburse sums already paid to the employee

Employers must have paid the full amount claimed for an employee’s wages to the employee before each claim is made. They should also pay the associated employee tax and employee and employer National Insurance contributions to HMRC, even if the company is in administration.

Employers cannot enter into any commitment or transaction with the employee which would reduce wages below the amount claimed (for example a salary sacrifice scheme). This includes any administration charge, fees or other costs in connection with the employment.

Where an employee had authorised their employer to make deductions from their net salary, these deductions can continue while the employee is working reduced hours provided that these deductions are not administration charges, fees or other costs in connection with the employment (for example, pension contributions and charitable giving).

Employees will be able to check if their employer has made a Job Support Scheme claim relating to them via their Personal Tax Account (sign up on GOV.UK).

Further details are available here.

Self-employed Grant

Are you Self-employed? Under the 3rd Self-Employment Income Support Scheme grant that covers Nov-Jan, you get 40% of profits, up to £3,750 for the 3 months.

This is less generous than grants 1 and 2, which covered 80% and 70% of profits respectively, although it’s double the 20% originally announced for the 3rd grant. There is no date yet for when you’ll actually be able to apply.

But there are stricter eligibility criteria and millions are still excluded. Crucially you’ll need to declare you have been affected by reduced demand to claim the 3rd grant. This is a significant change – with previous grants there were broader criteria and you could claim for any “adverse impact”.

Contact MCL Accountants on 01702 593 029 to optimise your tax position or if you need any assistance with your company accounts or job support scheme claims.

- ABOUT

- REQUEST A QUOTE

Ishan provides financial management, taxation and transactional advice to business entities of all sizes. His expert areas include statutory compliance, business taxation, personal tax & transactional processing and systems. Industry sectors include professional services, retail, hospitality and entertaining & media and advertising services.