New Dividend Reporting Rules from the 2025/26 Tax Year

From April 2025, directors must report detailed dividend information on Self-Assessment tax returns. Learn what’s changing and how to prepare.

Current tax tips and client-focused news, alongside a complete, searchable archive of past updates.

From April 2025, directors must report detailed dividend information on Self-Assessment tax returns. Learn what’s changing and how to prepare.

Making Tax Digital for Income Tax begins April 2026, requiring self-employed individuals and landlords to comply with digital tax reporting rules.

Discover how employers can claim a refund on overpaid PAYE tax, including eligibility, required documents, and submission methods via HMRC.

From April 2026, Making Tax Digital for Income Tax requires landlords and self-employed individuals to keep digital records and submit quarterly updates.

Autumn Budget 2024 was delivered by the Chancellor, Rachel Reeves on Wednesday, 30th October where she announced tax rises worth £40bn.

From 14 October 2024, HMRC requires taxpayers to provide evidence for PAYE employment expense claims using a P87 form, with digital claims resuming in 2025.

Are any funds lost through fraud Tax deductible is a question that comes up often these days due to the growing number of online scams & frauds.

Non-resident company landlord with UK property may be able to receive rental income with no tax deducted. Click to find out more.

Tax rises in October Budget has been a frequently asked question by our clients since the prime minister, Keir Starmer warned that the October Budget will be ‘painful’.

Changes to the taxation of non-UK domiciled individuals were announced by the new Chancellor in the Economic statement on 29 July 2024.

Learn how to choose an accountant or tax agent, ensuring they’re the right fit, as you’re still responsible for your own tax affairs.

National Insurance relief in UK Freeport or Investment Zone special tax sites is available to businesses that operate a business premises in a special tax site.

VAT on private school fees will be imposed by a Labour government as soon as practically possible should they win the next general election on 4th July.

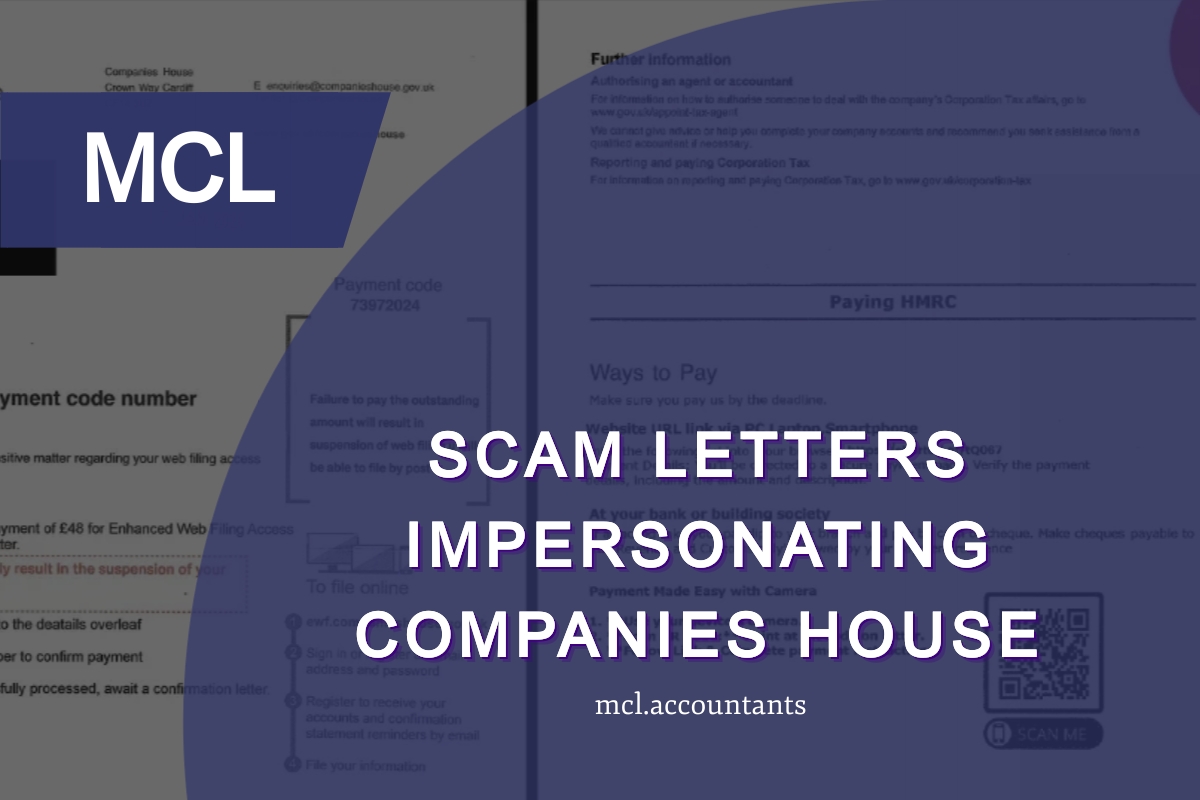

Scam letters impersonating Companies House have recently been received by clients who have set up new limited companies. Click to learn more.

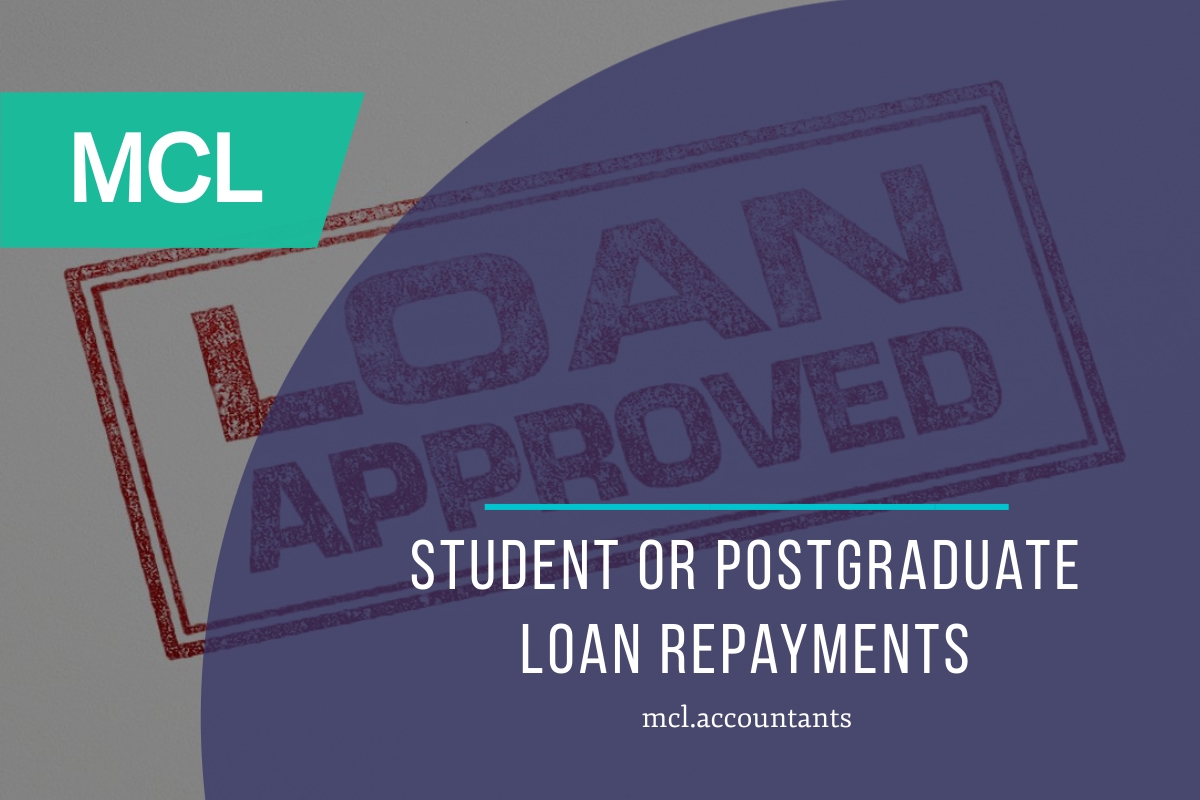

Student or postgraduate loan repayments are calculated as 9% of your total Self Assessment (SA) income above the threshold of your repayment plan type.